How Do You Read a Certificate of Insurance?

Reading a certificate of insurance might seem tricky at first, but it's easier once you understand the basics. Let's break down some of the most common terms you'll notice on a COI -especially on an ACORD 25 COI - and understand what they mean. Here's how to read a certificate of insurance:

Check out our Certificate of Insurance Walkthrough video and grab the sample COI provided below! For easy reference, we're using the Accord 25 form in our video because it's the most common form.

Feel free to watch the video above and download this sample coi below:

- Producer: The insurance agent or broker who supplied the policy

- Insured: The person, organization, or entity covered by the policy. Otherwise known as the “named insured.”

- Additional Insured: These endorsements cover people or entities in the event of claims and negligent acts. These parties usually have some degree of liability because of their relationship to the named insured.

- Coverages: Outlines the policies issued to the named insured

- General Liability: Covers liability if a business is sued for incidents that occur on its property, during or after completed operations, or because of its products

- Occurrence: One type of coverage protecting parties from incidents occurring during the policy period, regardless of when the claim is reported

- Claims-Made: Another type of coverage for claims that occur and reported within the policy period

- General Aggregate: The total amount an insurer is obligated to pay in a single term. They can respond in three ways: per policy, per project, and per location.

- Per Policy: The maximum amount an insurer pays for the total of all claims covered by an insurance policy

- Per Project: Limits applying to each of the policyholder’s projects (commonly used by building and retail store owners)

- Per Location: Limits applying to each of the policyholder’s locations (commonly used by companies and contractors doing project work, such as in construction trades)

- Automobile Liability: Covers policyholders who have suffered bodily injury or property damage from an auto accident that occurred on company property or with a company vehicle

- Auto insurance symbols include “Any Auto,” “Scheduled Autos,” “Hired Autos,” and “Non-Owned Autos.” “Any Auto” is most ideal because it means any vehicle the party drives will be covered.

- Umbrella & Excess Insurance:

- Excess Insurance: Does not expand policy terms, but includes higher coverage limits in case of unforeseen, catastrophic claims or loss

- Umbrella Insurance: A form of excess insurance that does expand policy terms and extends coverage to losses not outlined in the policy

- Workers’ Compensation & Employers Liability:

- Workers’ Compensation: Covers expenses resulting from workplace injuries, including medical care, lost wages, and rehabilitation

- Employers Liability: Pays for any lawsuits against employers resulting from employee injury or illness

- Other: Indicates if the named insured purchased other policies. This section is also where additional insured endorsements are listed.

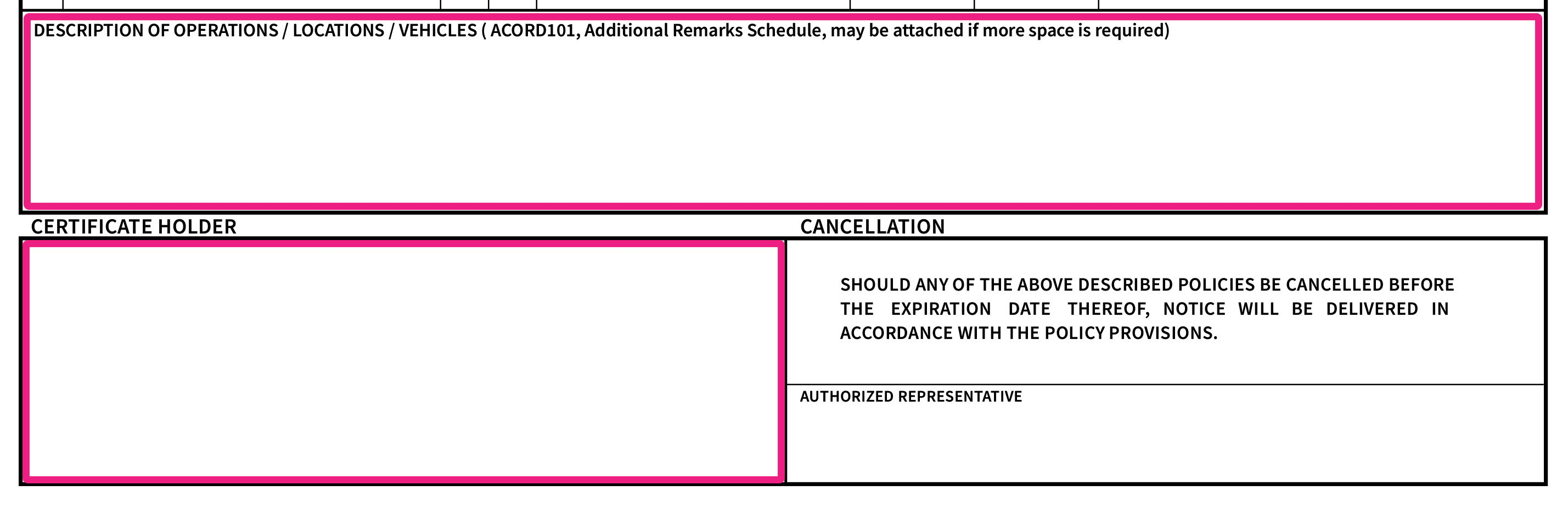

- Description of Operations/Locations/Vehicles/Exclusions Added by Endorsement/Special Provisions: Any special operations or job sites where work will take place. Additional insured endorsements are also listed here.

- Policy Number: The number assigned to the policy at the time it was issued

- Policy Effective Date: When a policy begins

- Policy Expiration Date: When a policy ends

- Certificate Holder: Entities a COI has been sent to or shared with

- Cancellation: The amount of notice an insurer will give the named insured if the policy is canceled before its expiration date

- Authorized Representative: Someone who has been given authority to sign the COI, whether an insurance agent, broker, or representative

What Is a Certificate Holder?

A Certificate holders is an individual or organization that is named on a certificate of insurance (COI) as having an interest in the insurance coverage provided by the policy.

When an insurance policyholder (often a business or individual) obtains a COI from their insurance provider, they can choose one or more certificate holders. The certificate holders may include entities such as clients, customers, landlords, vendors, or other parties with whom the policyholder has a contractual or legal relationship. By naming these entities as certificate holders, the policyholder provides them with proof of insurance coverage and notifies them of the details of the insurance policy.

The certificate holder is typically entitled to receive information about the insurance coverage, such as the policy limits, effective dates, and types of coverage provided. In the event of a claim or potential liability, the certificate holder may also be notified by the insurance provider and may have certain rights or obligations outlined in the insurance policy.

In commercial real estate, a certificate holder might be the landlord or property manager.

![]() Let’s say, for example, a kitchen cabinet subcontractor provides a business owner a copy of a COI to prove they are insured. The business owner would then be a certificate holder.

Let’s say, for example, a kitchen cabinet subcontractor provides a business owner a copy of a COI to prove they are insured. The business owner would then be a certificate holder.

These people or organizations are typically listed in the bottom left box of a COI labeled “Certificate Holder” or in the “Description of Operations/Locations/Vehicles/Exclusions Added by Endorsement/Special Provisions.”

While the certificate holder may be informed in advance of any policy cancellations, they don’t receive any other benefits or protection.

To return to our previous example, the business owner wouldn’t receive any added coverage or benefits from the kitchen cabinet subcontractor’s policy by being a certificate holder; only the policyholder and any additional insureds do.

Certificate holder vs. Additional Insured

In short: An additional insured has access to your insurance coverage and can file a claim if needed, while a certificate holder is only informed about your coverage but cannot file a claim. In simple terms, the additional insured is protected by your policy, whereas the certificate holder is not.

For a deeper understanding of the distinctions between additional insureds, policyholders, and certificate holders, we invite you to watch the informative video below.

What is the difference between COI and insurance policy?

While insurance policies are comprehensive documents reflecting your contract’s terms, coverage, and limits, certificates of insurance (COIs) are condensed versions of insurance policies.

COIs contain only the most essential aspects of these contracts with your insurance provider, such as the policyholder's name, effective and expiration dates, type of coverage, limits, and carrier. They do not modify coverage or alter the terms of the policy.

![]() For example, Paulina the Plumber is hired for a project in a skyrise by its property manager, Karl. To prove Paulina is insured, Karl asks her to provide a COI. While he doesn’t need the complete insurance policy, this abridged document verifies Paulina’s insured status so Karl can remain compliant.

For example, Paulina the Plumber is hired for a project in a skyrise by its property manager, Karl. To prove Paulina is insured, Karl asks her to provide a COI. While he doesn’t need the complete insurance policy, this abridged document verifies Paulina’s insured status so Karl can remain compliant.

It’s important to note that property owners and others requesting COIs do not receive additional policy benefits from it. Only if they are listed as additional insureds under these policies will coverage be extended to them in the event of a claim.

How Long Should I Keep a COI?

It's recommended to keep a certificate of insurance (COI) indefinitely for any vendors or third-party companies you work with, even after its expiration date.

After a COI expires, it's beneficial to retain it as a record of when your vendors were insured by a specific policy. Although the coverage period ends, the liability for incidents during that time may persist long after the project's completion. By keeping expired COIs, you can effectively manage liabilities associated with past projects or engagements.It is common practice to retain vendor COIs for at least the duration of the contract or agreement, plus a reasonable period thereafter. The length of time you should keep your vendor’s Certificate of Insurance (COI) depends on various factors, including contractual agreements, industry standards, and potential liability risks.Your company’s COI retention practice should be adjusted to the unique circumstances of your business, contractual obligations, and risk management considerations. Additionally, consult legal or compliance professionals for guidance on document retention requirements specific to your jurisdiction and industry.

![]()

For example, let’s say Rudy the Contractor accidentally uses harmful materials on a construction job site, but its effects don’t show up for years. Luckily, Peter the Property Manager, a small business owner, has been tracking COIs with an automated platform. So, when visitors to the building begin developing side effects and sue his business, Peter is able to access a copy of their COI from that time period, mitigate his own liability, and ensure those affected are compensated with the proper insurance coverage.

Archiving COIs can also come in handy during labor disputes regarding health insurance provisions, paid time off, and more to help an organization prove a contractor was not a full-time employee at the time of the incident.

For these reasons, a robust COI tracking process should include not only monitoring coverage for ongoing projects, but archiving documents from completed ones.

Why should I Track COIs?

Anyone who owns or operates a business, commercial property, or other site and works with third-party contractors should be tracking certificates of insurance (COIs).

These shortened documents reflecting all pertinent details of an insurance policy are key for reducing risks, ensuring compliance, and building safer business connections.

Depending on your company’s needs and bandwidth, you might choose to track COIs in-house or work with a team of insurance specialists. This is because tracking COIs is one of the most crucial aspects of any organization's risk management strategy. Let’s take a look at several key advantages of doing so:

Let’s take a look at several key advantages of doing so:

- Confirms vendor compliance with financial requirements

- Makes it easier to adjust claims in the event of a loss

- Minimizes insurance costs during audits and protects businesses against potentially millions in claims each year

- Ensures vendors are compliant and can continue working on job sites—improving productivity and project completion

- Minimizes coverage lapses via automated alerts about approaching policy end dates

- Provides valuable insights by highlight coverage gaps and centralizing data

- Mitigates evolving risks organizations face as vendors, project scopes, and conditions change over time

Verifying COI Compliance

When tracking COIs to verify vendor compliance, it's crucial to consider various factors such as contract requirements, insurance policies, and regulatory standards.

While assigning a knowledgeable individual to oversee COI collection and review can streamline the process, some teams may lack the bandwidth for such tasks. In such cases, partnering with dedicated COI tracking analysts can be beneficial. This collaborative approach not only reduces the risk of non-compliance but also minimizes guesswork and potential claims issues.

Whether you’re utilizing an Excel template or integrated software, keep in mind the following questions to ensure you’re tracking COIs correctly:

- Is keeping this process internal saving my company money?

- Could our employees be better using their time to accomplish other projects and work that contributes to our bottom line?

- Do I know how compliant my vendors are?

- Do we have team members who are comfortable enough with insurance terminology to correct deficiencies and manage compliance?

- Will our current COI tracking process be able to accommodate hundreds or even thousands more vendors if the company grows?

Tracking COIs In-House

Tracking COIs in-house is accompanied by several important considerations.

Whether you’re utilizing an Excel template or integrated software, keep in mind the following questions to ensure you’re tracking COIs correctly:

- Is keeping this process internal saving my company money?

- Could our employees be better using their time to accomplish other projects and work that contributes to our bottom line?

- Do I know how compliant my vendors are?

- Do we have team members who are comfortable enough with insurance terminology to correct deficiencies and manage compliance?

- Will our current COI tracking process be able to accommodate hundreds or even thousands more vendors if the company grows?

If you’re tracking COIs in-house, consider using the following free resources:

- The International Risk Management Institute (IRMI)

- bcs University

- Email & Task Manager Platforms

- QuickBooks

- bcs's Certificate of Insurance Tracking Template

You can also try bcs's COI tracking software for FREE.

Finding the Best COI Tracking Solution

If you decide to work with a COI tracking provider, the next question is: Do you need a full-service or self-service solution?

- Self-service tracking includes robust software your team can use to store, manage, and track COIs. However, while these intuitive platforms help streamline compliance and safeguard vendor information, they require staff to manage them.

- Full-service solutions come equipped with a team of insurance specialists to handle every facet of COI tracking for you. Along with the benefits of managing these processes in a secure environment, full-service tracking provides access to dedicated compliance expertise so you can free up your teams, mitigate risks, and enable projects to run smoothly.

To decide whether self- or full-service COI tracking is right for you, consider the following factors:

- Self Service:

- Small Businesses

- Low, Manageable Vendor Volume

- Sufficient In-House Insurance Knowledge

- Full Service:

- Medium-to-Large or Growing Businesses

- Large Vendor Volume

- Hands-On Approach & Expertise

Is There Free COI Tracking?

Businesses often seek cost-effective solutions to manage their COI tracking processes. While many may consider handling these tasks in-house to save on expenses, it's essential to recognize that no COI tracking solution is entirely free.

When managing COIs internally, team members must invest time and resources that could otherwise be allocated to revenue-generating activities. As companies grow and engage with more vendors, these tasks become increasingly time-consuming.

Outsourcing COI tracking to a dedicated solution incurs costs associated with software usage and access to expert support. However, to address the need for a budget-friendly option, we're excited to introduce our new Freemium version of COI tracking software.

Our Free Certificate of Insurance Tracking software, allows you to experience the benefits of our platform without immediate financial commitment. While the Freemium version provides valuable functionalities, such as COI tracking and vendor compliance management, it does have limitations, such as a restricted number of accounts or features.

We invite you to test our user-friendly COI tracking and vendor compliance software for free and discover how it can streamline your processes while ensuring compliance and mitigating risks. Take the first step toward improving your COI management today and experience the benefits firsthand.

To determine how much your current COI tracking solution is costing you we encourage you to use our free ROI calculator tool.

To gauge how much your current solution is costing you, use our free ROI calculator tool.

In addition, there are several free tools you can use to support in-house tracking, including:

- The International Risk Management Institute (IRMI)

- bcs university

- Email & Task Manager Platforms

- QuickBooks

- Professionally-Made Spreadsheets