How to Boost Your Claims Management Success

In July 2019, a Philadelphia federal appeals court ruled Amazon could be held liable for goods sold by third-party entities on its site. Though vacated pending a rehearing at the behest of the the e-commerce giant, the potential liabilities posed by such a finding highlights the threats third-party affiliations pose to businesses, and underscores the importance of stellar risk management. Companies should be proactive in ensuring they and their vendors are properly insured and protected to avoid vulnerability.

These six simple steps can help mitigate liabilities and guarantee desired claims management outcomes should you or subcontractors face similar challenges:

1. Have Your Own Policy

First and foremost, have your own comprehensive commercial general liability insurance policy to fall back on in case you miss a clause in your vendor’s policy holding you responsible for all or a portion of losses or damages in the case of an incident. Decide whether an occurrence policy or claims-made policy with tail coverage—both of which offer forms of lifetime coverage for events occurring during the policy period—is right for your company.

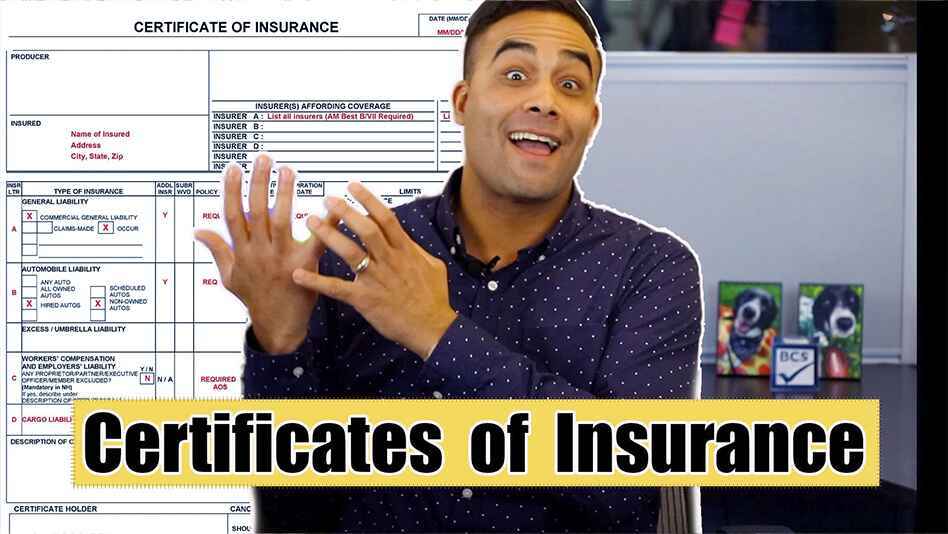

2. Request a Certificate of Insurance

A business should request a certificate of insurance (COI) from a vendor or subcontractor during the bidding process and before contracts are signed. The COI serves as an insurance policy summary, provides quick access to the information, reduces culpability, and protects your company from potential claims and litigation.

Request the COI directly from the insurance company to validate coverage. Also, check the name on the certificate is an exact match to the insured contractor and policy dates are in effect.

Read the Guide to Certificates of Insurance for more information.

3. Include an Indemnity Clause in the Contract

An indemnity clause, also known as hold harmless, is an essential section to include in a contract, because it transfers risk from one party (your company) to another (the vendor) in the event of losses or damages. The clause ensures the vendor is liable out of pocket or through insurance for your company’s misfortunes.

While the vendor may have the financial means to “make good” on the damages, requiring them to have insurance guarantees your company will be compensated.

4. Review Vendor Insurance

To reduce and successfully resolve claims made against vendors and your organization, review the vendor’s insurance and umbrella or excess liability policies carefully, and check it meets certain criteria.

First, verify the vendor is the Named Insured and your company is identified as the Additional Insured to extend coverage to your company for the acts of the vendor. Because there are thousands of Additional Insured endorsement variations in circulation, confirm it provides the desired risk transfer. Require your Additional Insured status be “primary and noncontributory,” which establishes the vendor’s policy will pay damages on behalf of your company for a covered claim and won’t seek your company’s policy to contribute to the claim’s defense or settlement.

Check the vendor’s insurer has an A.M. Best, one of the oldest rating providers, financial strength rating of at least A-, and financial size rating minimum of VII ($50 million to $100 million in assets).

Next, review the effective and expiration dates, the type of insurance (occurrence or claims-made), notice of cancellation, and the limits, which are set for each occurrence, general aggregate, products/completed operations aggregate, personal and advertising injury, damage to premises rented to you, and medical expenses.

Another layer of protection is the waiver of subrogation, a provision preventing vendors and their insurance companies from recovering any or all payment for losses that may be attributed to your company’s negligence.

Download the 9 Fundamentals of Vendor Insurance Review to learn more.

5. Track & Manage Compliance

The vendor insurance review process never ends. After an initial assessment, certificates of insurance should be tracked and continuously monitored for changes to limit burdens, prevent a lapse in coverage, and guarantee compliance.

To track COIs, your company must develop a collection, analyzation, correction, and follow-up process, which can be completed manually or through certificate of insurance tracking software such as the bcs app. Because managing these documents by hand can be laborious, time consuming and prone to errors, utilize technology that offers accuracy, customization, integration options, real-time data, accessibility, analytics, and security.

6. Clear Communication

Having open and clear communication through the contract process and beyond will establish expectations and ensure they are met. Outline your insurance criteria, operational guidelines, and government regulations in the vendor compliance policy. Reiterate these standards in contracts and throughout the relationship with subcontractors. Always follow up on changes or cancellations in policies with both the policyholder and insurer.

How BCS Helps

Business Credentialing Services provides all of the tools necessary to mitigate insurance risks and boost your claims management success. The self-service option provides a convenient software platform, and the full-service solution includes a team of compliance analysts and the technology to track certificates of insurance through collection, error identification, review, and correction. Other services include regulatory screening, pre-safety qualification, and financial screening.

Subscribe Now

Learn from the pros about risk-mitigation, document tracking, and more, with expert articles from bcs.

Leave a comment